MORE FREE TERM PAPERS MANAGEMENT:

|

||||||||||||||||||||||||||

IMPORTANCE OF SERVICE SECTOR IN INDIA

SERVICE SECTOR

The tertiary sector of the economy (also known as the service sector or the service industry) is one of the three economic sectors, the others being the secondary sector(approximately the same as manufacturing) and the primary sector (agriculture, fishing, and extraction such as mining).

The service sector consists of the "soft" parts of the economy, i.e. activities where people offer their knowledge and time to improve productivity, performance, potential, and sustainability. The basic characteristic of this sector is the production of services instead of end products. Services (also known as "intangible goods") include attention, advice, experience, and discussion. The production of information is generally also regarded as a service, but some economists now attribute it to a fourth sector, the quaternary sector.

The tertiary sector of industry involves the provision of services to other businesses as well as final consumers. Services may involve the transport, distribution and sale of goods from producer to a consumer, as may happen in wholesaling and retailing, or may involve the provision of a service, such as in pest control or entertainment. The goods may be transformed in the process of providing the service, as happens in the restaurant industry. However, the focus is on people interacting with people and serving the customer rather than transforming physical goods.

For the last 30 years there has been a substantial shift from the primary and secondary sectors to the tertiary sector in industrialized countries. The tertiary sector is now the largest sector of the economy in the Western world, and is also the fastest-growing sector.

Services or the "tertiary sector" of the economy covers a wide gamut of activities like trading, banking & finance, infotainment, real estate, transportation, security, management & technical consultancy among several others. The various sectors that combine together to constitute service industry in India are:

• Trade

• Hotels and Restaurants

• Railways

• Other Transport & Storage

• Communication (Post, Telecom)

• Banking

• Insurance

• Dwellings, Real Estate

• Business Services

• Public Administration; Defence

• Personal Services

• Community Services

• Other Services

Services Sector in Indian Economy

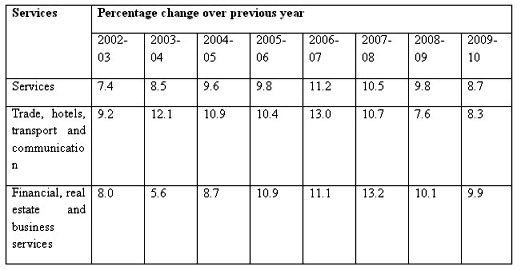

Contribution of Services Sector to Indian Economy:The high growth rate achieved by the Indian economy over the last decade or so has much to owe to the Services sector. Services have contributed around 68.6% of the overall average growth in the GDP in the period from 2002-2003 to 2006-2007. Unlike the manufacturing and agriculture sectors, Services growth has been broad-based and has shown a positive incremental growth since 2000-01. Trade, hotels, transport and communications services had clocked a double-digit growth during the aforementioned four year period. The Economic Survey 2010 recognised the importance of the sector by stating “For more than a decade now India’s services sector has been the powerhouse of the nation’s economic growth. This is also a sector that now produces more than half the GDP of the nation.” In the period 2000-06, according to the Central Statistical Organisation of India, services contributed 58% of India’s GDP. Thus the Indian economy over the years has become increasingly dependent on the services sector for its growth performance. These numbers most likely understate the overall importance of services for the economy as many services provide inputs to the production process and to other sectors and thus their growth has wider productivity and efficiency ramifications for activities outside of the services sector.

Table 1- Growth of Services Sector in India (in %)

EXPORTS OF SERVICES

Services contribute significantly to India’s integration with world markets through trade and FDI flows. India has been recording high growth in the export of services during the last few years. As per RBI’s data, India’s services exports grew from US$ 17 billion in 2001-02 to around US$ 102 billion in 2008-09.Growth has been particularly rapid in the miscellaneous service category, which comprises of software services, business services, financial services and communication services.

In 2005, while India’s share and ranking in world merchandise exports were 0.9% and 29th, respectively, its share and ranking in world commercial services’ exports was 2.3% and 11th, respectively. In 2008, India’s share and ranking in world commercial services’ exports improved to 2.7% and 9th, respectively

Services exports have grown much faster than merchandise exports and corresponded to 57% of merchandise exports in 2008-09. The share of services in India’s total exports has increased from 7% in 1999-2000 to 37% in 2008-09 suggesting its growing importance in India’s overall export basket.

Employment in Services Sector

At present services account for about 26 per cent of total organized sector employment in the country while contributing a little over 55 per cent to the national GDP. A sectoral disaggregation of the employed workforce shows that the contribution to employment of services (excluding construction) rose from 22.8 to 23.4 per cent, while the workforce increased from 397.0 to 457.8 million between 1999-2000 and 2004-05 (details in Table 1c below). Out of the increase in workforce by 60.8 million, the incremental share of services was 16.8 million. However, despite the low overall elasticity of employment in the country (at just 0.48) and not only in the services sector, the latest NSSO data shows that employment elasticity is reasonably high (and increasing) in certain services categories, with financing, insurance, real estate and business services registering an elasticity of employment of 0.94 followed by construction sector employment elasticity at 0.88.FOREIGN DIRECT INVESTMENT IN SERVICE SECTOR IN INDIA:

There is good news for India Inc. Despite the global financial crisis, inflow of foreign capital to the country has increased sharply in 2008. The aggregate inflow of foreign direct investment (FDI) has more than doubled in 2008 over 2007. The stake was enormous. For, Corporate India’s dependence on foreign funds has increased steadily in recent years as the easing of norms for FDI, especially, external commercial borrowings (ECB), over the years had led to a dramatic rise in the inflow of foreign capital in India.

Granted, there are reasons for caution as these data relate to 2008 only and the situation may have changed in 2009. After all, the crisis is not over yet. In fact, RBI’s recent release shows that the inflow of ECB and foreign currency convertible bonds (FCCBs) has slowed down considerably in 2009 — down 73% from $1,702 million in November 2008 to $453 million in February 2009.

The decline in ECB is feared to affect the investment plans of companies. After all, a large number of companies use these funds to import capital goods . In fact, of the 32 companies which raised funds through ECB and FCCBs last February through the automated route, as many as 15 did so for import of capital goods for expansion of capacity or for modernisation of plants.

That India’s investment activities in recent years have largely been financed by foreign sources may be seen in the sharp rise in FDI inflows. Aggregate inflow of FDI has increased more than nine times during the past five years, from Rs 14,781 crore in 2004 to Rs 1,39,725 crore in 2008.

While improved macro fundamentals in recent years have strengthened the confidence of foreign investors in Indian industry, opening up of new areas and changes in government policy towards FDI must have engineered this jump in foreign capital inflow. That opening up of new areas has given foreign investors more investment options is reflected in the changing destinations of foreign capital. The service sector, which was a restricted domain for foreign capital in the past, for example, has become the most sought-after area of late.

The service sector has been the prime mover of India’s gross domestic product in recent years and foreign investors never had doubts about its potential. However, policy restrictions in the past did not allow them to invest in this industry as much as they willed. Now that restrictions have been eased, FDI has flowed in to this industry as never before

.

It accounted for a huge 24.3% of the total FDI inflow in 2008. In actual terms, the FDI inflow to this sector has grown 32 times in the past five years from a mere Rs 1,074 crore in 2004 to Rs 33,947 crore in 2008.The second most important destination of FDI in 2008 was telecommunication. It accounted for about 8.3% of the total FDI flowing into the country in 2007.

But while the service sector and the telecommunication industry have increased their share in total FDI inflows in the country in 2008, the software industry has gone down the ladder further. The poor performance of the software companies dampened the mood of the foreign investors and FDI inflow to software sector has fallen sharply.

The sector received only Rs 7,810 crore FDI in 2008 against Rs 10,214 crore in 2007. Its share in total FDI inflow has fallen to only 5.6% in 2008 against 16% in 2007. But as the financial crisis continues, the big question is: Will FDI inflow to India grow at the same rate in the coming months?

After all, the service sector, which has been the main contributor to GDP growth, was the biggest gainer of the rise in FDI inflow in recent years. Now if the FDI inflow slows down, it will affect the growth of the service sector and in turn, the GDP growth.

DIFFERENT SERVICE SECTORS IN INDIAIT SECTOR IN INDIA

Information technology essentially refers to the digital processing, storage and communication of information of all kinds . Therefore, IT can potentially be used in every sector of the economy. The true impact of IT on growth and productivity continues to be a matter of debate, even in the United States, which has been the leader and largest adopter of IT. However, there is no doubt that the IT sector has been a dynamic one in many developed countries, and India has stood out as a developing country where IT, in the guise of software exports, has grown dramatically, despite the country’s relatively low level of income and development. An example of IT’s broader impact comes from the case of so-called IT-enabled services, a broad category covering many different kinds of data processing and voice interactions that use some IT infrastructure as inputs, but do not necessarily involve the production of IT outputs. India’s figures for the size of the IT sector typically include such services.

The share of banking and insurance services in the GDP of India has been stable between 5.5 and 6.5 per cent over the last few years even though the sector has been showing a double digit growth in the pre-2008 period. Even the impact of the economic slowdown was considerably managed owing to the strong and conservative adherence to prudential norms under Basel II even as the industry met its social sector targets. The following sections lay out the contours of the regulatory system in the financial sector in India.

The financial sector reforms in India since the early 1990s have resulted in a robust banking system where existing financial institutions operated in an environment of operational flexibility and functional autonomy even as financial system was made consistent with the movement towards global integration of financial services. The strong regulatory system India has put in place to govern its financial sector greatly contributed in weathering the ongoing financial crisis.

In February 2005, the Government of India and the Reserve Bank released the ‘Roadmap for Presence of Foreign Banks in India’ laying out a two-track and gradualist approach aimed at increasing the efficiency and stability of the banking sector in India. One track was the consolidation of the domestic banking system, both in private and public sectors, and the second track was the gradual enhancement of the presence of foreign banks in a synchronised manner. The roadmap was divided into two phases, the first phase spanning the period March 2005 - March 2009, and the second phase beginning April 2009 after a review of the experience gained in the first phase.

As per the Phase-I of the road map, foreign banks have been permitted to hold a total of 74 per cent foreign equity in Indian private banks, while there has been an aggregate cap of 20 per cent for Indian public sector banks. However individual foreign banks are restricted to holding less than 5 per cent equity of any one bank, unless a bank is identified for restructuring. During this phase, permission for acquisition of share holding in Indian private sector banks by eligible foreign banks will be limited to banks identified by RBI for restructuring. RBI may if it is satisfied that such investment by the foreign bank concerned will be in the long term interest of all the stakeholders in the investee bank, permit such acquisition. Where such acquisition is by a foreign bank having presence in India, a maximum period of six months will be given for conforming to the ‘one form of presence’ concept.During the first phase foreign banks will be permitted to establish presence by way of setting up a wholly owned banking subsidiary (WOS) or conversion of the existing branches into a WOS. To facilitate this, RBI has also issued detailed guidelines. The guidelines cover, inter alia, the eligibility criteria of the applicant foreign banks such as ownership pattern, financial soundness, supervisory rating and the international ranking].

It is worth noting that for non-banking finance companies (NBFC), FDI up to 100 per cent is allowed automatically subject to minimum capitalization norms. In respect of NBFCs in India, 19 areas have been opened for FDI including portfolio management services, stock broking, credit rating agencies, housing finance and rural credit among others. In the insurance sector in India, foreign equity up to 26 per cent is allowed.

India has a WTO commitment to allocate 12 new bank branch licences per year to foreign banks, subject to a minimum initial capital requirement. The grant of a licence to operate an ATM is not counted in the WTO commitment of 12 bank branches of foreign banks. The grant of ATM is governed by the Branch authorisation policy of September 2005. There are more than 280 foreign bank branches in India and more than 800 ATM’s of foreign banks in India. The WOS will be treated on par with the existing branches of foreign banks for branch expansion with flexibility to go beyond the existing WTO commitments of 12 branches in a year and preference for branch expansion in under-banked areas.

The second phase of the roadmap was to commence from April 2009. In view of the current global financial market turmoil, there are uncertainties surrounding the financial strength of banks around the world. Further, the regulatory and supervisory policies at national and international levels are under review. In view of this, it is considered advisable, for the time being, to continue with the current policy and procedures governing the presence of foreign banks in India. The proposed review will be taken up after due consultation with the stakeholders once there is greater clarity regarding stability, recovery of the global financial system, and a shared understanding on the regulatory and supervisory architecture around the world.

Implemented reforms have led to a significant improvement in public sector banks performance. The introduction of best international practices and norms, refinements in the supervisory practices, tightening of risk weights/provisioning norms in regard to sectors witnessing high credit growth, market discipline brought about by listing on the stock exchanges and interest rate deregulation are key factors in this improved performance. Simultaneously, greater competition has been induced with the introduction of new generation private sector banks. Notwithstanding the progress made since the early 1990s, the Reserve Bank of India has publicly stated that domestic financial markets need to develop further, particularly so as to support accelerated economic growth within India.While India has opened up many of its financial services, India has always followed a cautious approach as a result of its capital account not being fully open. While India subscribes to the Annex on Financial Services, it is not a party to the Understanding on Financial Services.

INDIAN TELECOM SECTOR:

The telecom services have been recognized the world-over as an important tool for socio-economic development for a nation. It is one of the prime support services needed for rapid growth and modernization of various sectors of the economy. Indian telecommunication sector has undergone a major process of transformation through significant policy reforms, particularly beginning with the announcement of NTP 1994 and was subsequently re-emphasized and carried forward under NTP 1999. Driven by various policy initiatives, the Indian telecom sector witnessed a complete transformation in the last decade. It has achieved a phenomenal growth during the last few years and is poised to take a big leap in the future also.

The Indian Telecommunications network with 621 million connections (as on March 2010) is the third largest in the world. The sector is growing at a speed of 45% during the recent years. This rapid growth is possible due to various proactive and positive decisions of the Government and contribution of both by the public and the private sectors. The rapid strides in the telecom sector have been facilitated by liberal policies of the Government that provides easy market access for telecom equipment and a fair regulatory framework for offering telecom services to the Indian consumers at affordable prices. Presently, all the telecom services have been opened for private participation. The Government has taken following main initiatives for the growth of the Telecom Sector.

Foreign Direct Investment In Telecom Sector:

In Basic, Cellular Mobile, Paging and Value Added Service, and Global Mobile Personal Communications by Satellite, Composite FDI permitted is 74% (49% under automatic route) subject to grant of license from Department of Telecommunications subject to security and license conditions. (para 5.38.1 to 5.38.4 of consolidate FDI Policy circular 1/2010 of DIPP)

FDI upto 74% (49% under automatic route) is also permitted for the following: -

• Radio Paging Service

. Internet Service Providers (ISP's)

FDI upto 100% permitted in respect of the following telecom services: -

• Infrastructure Providers providing dark fibre (IP Category I);

• Electronic Mail; and

• Voice Mail

Subject to the conditions that such companies would divest 26% of their equity in favor of Indian public in 5 years, if these companies were listed in other parts of the world. In telecom manufacturing sector 100% FDI is permitted under automatic route.

The Government has modified method of calculation of Direct and Indirect Foreign Investment in sector with caps(para 4.1 of consolidate FDI Policy circular 1/2010 of DIPP) and have also issued guidelines on downstream investment by Indian Companies. (para 4.6 of consolidate FDI Policy circular 1/2010 of DIPP)

Guidelines for transfer of ownership or control of Indian companies in sectors with caps from resident Indian citizens to non-resident entities have been issued (para 4.2.3 of consolidate FDI Policy circular 1/2010 of DIPP)

BANKING AND INSURANCE:

The share of banking and insurance services in the GDP of India has been stable between 5.5 and 6.5 per cent over the last few years even though the sector has been showing a double digit growth in the pre-2008 period. Even the impact of the economic slowdown was considerably managed owing to the strong and conservative adherence to prudential norms under Basel II even as the industry met its social sector targets. The following sections lay out the contours of the regulatory system in the financial sector in India.

The financial sector reforms in India since the early 1990s have resulted in a robust banking system where existing financial institutions operated in an environment of operational flexibility and functional autonomy even as financial system was made consistent with the movement towards global integration of financial services. The strong regulatory system India has put in place to govern its financial sector greatly contributed in weathering the ongoing financial crisis.

In February 2005, the Government of India and the Reserve Bank released the ‘Roadmap for Presence of Foreign Banks in India’ laying out a two-track and gradualist approach aimed at increasing the efficiency and stability of the banking sector in India. One track was the consolidation of the domestic banking system, both in private and public sectors, and the second track was the gradual enhancement of the presence of foreign banks in a synchronised manner. The roadmap was divided into two phases, the first phase spanning the period March 2005 - March 2009, and the second phase beginning April 2009 after a review of the experience gained in the first phase.

As per the Phase-I of the road map, foreign banks have been permitted to hold a total of 74 per cent foreign equity in Indian private banks, while there has been an aggregate cap of 20 per cent for Indian public sector banks. However individual foreign banks are restricted to holding less than 5 per cent equity of any one bank, unless a bank is identified for restructuring. During this phase, permission for acquisition of share holding in Indian private sector banks by eligible foreign banks will be limited to banks identified by RBI for restructuring. RBI may if it is satisfied that such investment by the foreign bank concerned will be in the long term interest of all the stakeholders in the investee bank, permit such acquisition. Where such acquisition is by a foreign bank having presence in India, a maximum period of six months will be given for conforming to the ‘one form of presence’ concept.During the first phase foreign banks will be permitted to establish presence by way of setting up a wholly owned banking subsidiary (WOS) or conversion of the existing branches into a WOS. To facilitate this, RBI has also issued detailed guidelines. The guidelines cover, inter alia, the eligibility criteria of the applicant foreign banks such as ownership pattern, financial soundness, supervisory rating and the international ranking].

It is worth noting that for non-banking finance companies (NBFC), FDI up to 100 per cent is allowed automatically subject to minimum capitalization norms. In respect of NBFCs in India, 19 areas have been opened for FDI including portfolio management services, stock broking, credit rating agencies, housing finance and rural credit among others. In the insurance sector in India, foreign equity up to 26 per cent is allowed.

India has a WTO commitment to allocate 12 new bank branch licences per year to foreign banks, subject to a minimum initial capital requirement. The grant of a licence to operate an ATM is not counted in the WTO commitment of 12 bank branches of foreign banks. The grant of ATM is governed by the Branch authorisation policy of September 2005. There are more than 280 foreign bank branches in India and more than 800 ATM’s of foreign banks in India. The WOS will be treated on par with the existing branches of foreign banks for branch expansion with flexibility to go beyond the existing WTO commitments of 12 branches in a year and preference for branch expansion in under-banked areas.

The second phase of the roadmap was to commence from April 2009. In view of the current global financial market turmoil, there are uncertainties surrounding the financial strength of banks around the world. Further, the regulatory and supervisory policies at national and international levels are under review. In view of this, it is considered advisable, for the time being, to continue with the current policy and procedures governing the presence of foreign banks in India. The proposed review will be taken up after due consultation with the stakeholders once there is greater clarity regarding stability, recovery of the global financial system, and a shared understanding on the regulatory and supervisory architecture around the world.

Implemented reforms have led to a significant improvement in public sector banks performance. The introduction of best international practices and norms, refinements in the supervisory practices, tightening of risk weights/provisioning norms in regard to sectors witnessing high credit growth, market discipline brought about by listing on the stock exchanges and interest rate deregulation are key factors in this improved performance. Simultaneously, greater competition has been induced with the introduction of new generation private sector banks. Notwithstanding the progress made since the early 1990s, the Reserve Bank of India has publicly stated that domestic financial markets need to develop further, particularly so as to support accelerated economic growth within India.While India has opened up many of its financial services, India has always followed a cautious approach as a result of its capital account not being fully open. While India subscribes to the Annex on Financial Services, it is not a party to the Understanding on Financial Services.

EDUCATION SECTOR:

Education levels have a direct bearing on the sustainability of a country’s competitiveness and economic growth. Against the background of economic globalisation, the development of human capital very much depends on the internationalisation of education services.The Indian Constitution places Education under the twin jurisdiction of both the State and the Central Governments. However, technical and higher education sectors are regulated by the All India Council for Technical Education (AICTE) Act and the University Grants Commission (UGC) Act, respectively. Though, there is no current regulatory framework in India which allows foreign tertiary education providers to deliver courses in India (apart from in relation to technical education), a new legislation on entry of foreign higher and technical education institutions, is under consideration. The current legal interpretation of the extant constitutional provisions puts education as a non-commercial activity. Yet, at present, foreign investment is allowed in institutes of higher education and technical training, but only on a franchisee and affiliation basis. Both the UGC and the AICTE seek to regulate the entry and operation of foreign educational institutions in India. Technical institutions need to obtain accreditation from AICTE.

Professional and vocational courses have attracted many foreign education service providers especially in niche areas such as business and hotel management, engineering, medicine, fashion design, etc. on a franchisee and affiliation basis.

The Government of India through the Ministry of Human Resources Development has actively encouraged foreign students to come to India to pursue higher studies.

Primary and secondary education sectors do not find such open regimes especially because of the emphasis on nation-building in school curricula. Even so, international schools, if allowed, are permitted 100 per cent foreign direct investment under the automatic route, subject to certain domestic regulations and norms being followed.

A possible bilateral FTA could:

facilitate access for researchers engaged in short/long term work of a collaborative nature;

explore the ways to facilitate the recognition of qualifications in both countries by their concerned organisations;

improve access for education services providers seeking to operate in each other’s market, particularly in vocational education; and

facilitate greater transparency in approval and accreditation processes for education service providers.

PROFESSIONAL SERVICES:

Professional services include the widest variety of individual and firm based services. These include, inter alia, legal, accountancy, engineering, architecture and medical services. This set of services is amenable to all the four modes of supply recognised under GATS.

Expansion in trade in professional services has the maximum forward and backward linkages in deepening of commercial relationships between countries. It also is one of the most rapid methods of dissemination of knowledge and skills, and consequently of technology across borders.

Trade in professional services requires the ability of the professional to render the relevant service to be objectively measured. This is achieved through mutual recognition of qualifications. Additionally, professionals may be required to be registered with the local professional associations or guilds to be allowed to render the relevant service in the concerned jurisdiction.

These guilds or associations are largely self-governed and the government plays a limited role even if the profession may be regulated by statute. Governments can, however, decide the conditions, if any, under which foreign professionals can enter the host country and the extent to which they can provide the service. In addition, the Governments also would be required to either make and notify or vet and notify the domestic regulations regarding the services.

Professional bodies do seek mutual recognition agreements (MRAs) with their counterparts in other countries, sometimes without Government intervention. MRAs can be very complex, and so need to be carefully drafted and negotiated. A simple MRA is one where registration with the relevant professional body in one country would be recognised for the purposes of automatic registration with the counterpart in the other country.

India has included domestic regulation provisions in its Comprehensive Trade Agreements with Singapore and Korea, which contains articles which mirror the relevant GATS provisions (Article VI.2-4). In sectors where specific commitments regarding professional services are undertaken, it has been agreed to provide for adequate procedures to verify the competence of professionals of the other country.

ENGINEERING SERVICES:

In the case of engineering and integrated engineering services, India has the single largest pool of technically qualified and trained manpower with the potential to operate in the international market. With the growth in the manufacturing and services sector, and given the aging demographic profile of most developed countries, the demand for Indian engineers is likely to increase considerably in the coming years.

Further, given the widespread expansion of the telecommunications sector and the increasing digitization of various services, there is great potential in export of engineering services through mode 1. According to NASSCOM, India’s share of the USD 10-15 billion worth of engineering services off-shored was estimated at around 12%.

In order to enable Indian engineers to practice their professions and make careers in foreign countries with ease, India, represented by the All India Council for Technical Education (AICTE), has become a provisional member of the Washington Accord which is a 10 member-nation apex global organisation that determines standards of Engineering Education. This ensures that Indian undergraduate engineering degrees would be accorded an equal status in all member countries and they are recognized as engineering degrees of high international standards.CONSTRUCTION SECTOR:

In the case of engineering and integrated engineering services, India has the single largest pool of technically qualified and trained manpower with the potential to operate in the international market. With the growth in the manufacturing and services sector, and given the aging demographic profile of most developed countries, the demand for Indian engineers is likely to increase considerably in the coming years.

Further, given the widespread expansion of the telecommunications sector and the increasing digitization of various services, there is great potential in export of engineering services through mode 1. According to NASSCOM, India’s share of the USD 10-15 billion worth of engineering services off-shored was estimated at around 12%.

In order to enable Indian engineers to practice their professions and make careers in foreign countries with ease, India, represented by the All India Council for Technical Education , has become a provisional member of the Washington Accord which is a 10 member-nation apex global organisation that determines standards of Engineering Education. This ensures that Indian undergraduate engineering degrees would be accorded an equal status in all member countries and they are recognized as engineering degrees of high international standards.HEALTH SERVICES:

India is in a position to tap the top end of the USD 3 trillion global healthcare market because of the quality of its services and the brand equity of Indian healthcare professionals across the globe. The Indian Government places top priority on the healthcare sector and is focusing on indigenous research and development and the further creation of human capital.

It is expected that the Indian laws and procedures relating to recognition of intellectual property and foreign investments will allow global pharmaceuticals and biotechnology companies to set up partnerships with Indian counterparts.

The Indian Healthcare is a US$ 35 billion industry in India, expected to reach over US$ 75 billion by 2012, US$ 150 billion by 2017. India has developed a brand name in supply of quality healthcare services at relatively cheaper rates compared to the USA, UK and rest of Europe. With a large pool of highly qualified doctors, nurses, paramedics and technicians and with growing innovations, expansions, low cost of treatment, world-class technology and five-star services not just in the western system of medicine but also in indigenous systems, including Ayurveda, Yoga & Naturopathy, Unani, Siddha and Homoeopathy, offering holistic health care, medical tourism is growing at a phenomenal rate of 30-35 per cent in India. India, with a large pool of well trained and highly qualified, English proficient health care professionals available at highly competitive rates, has a comparative advantage in export of health services through mode 4. Also, with rapid progress in information and communications and technology, it is noted that a large part of health care services is being traded internationally through mode 1.

There is potential for cooperation between Turkey and India in joint training programmes for human resource development and sharing of information and experience in respect of health industry best practice. To facilitate movement of healthcare students both countries may investigate the feasibility of facilitating mutual recognition arrangements for the recognition of degrees in the field of doctors, nurses and trained health technicians. The FTA would also provide opportunities for cooperation in healthcare services.

Public institutions played a dominant role in the Indian Healthcare sector in the past, in the urban as well as in the rural areas. However, the public healthcare has been on a serious decline during the last two or three decades because of non-availability of medical and paramedical staff, diagnostic services and medicines. Consequently there has been a pronounced decline in the percentage of cases of hospitalized treatment in Government hospitals and a corresponding increase in the percentage treated in private hospitals, despite higher costs in the private sector.The Group is of the view that it is imperative for the health and safety of the population to enforce minimum standards on clinical establishments in both the private and public sectors by laying down minimum standards and enforcing them rigorously. The Clinical Establishments (Registration and Regulation) Bill, 2007 having been introduced in the Parliament it would important to ensure that it becomes law at the earliest and that it enters into force for all the States. The next step would be for the proposed National Committee to set appropriate standards for all categories of clinical establishments.

TOURISM SECTOR:

Tourism is estimated to contribute 5.83 per cent to the GDP and 8.27 per cent to employment in the country; the employment generated by tourism is estimated at 51.1 million in 2006-07. In 2006, foreign tourist arrivals (business travellers, leisure travellers and persons of Indian origin holding foreign passports) had increased to 4.42 million, while the number of domestic tourists as reported by the Ministry of Tourism was 462 million. However, the Revealed Comparative Advantage (RCA) of India in travel services has been on the decline.

It is estimated that the shortfall in tourist accommodation in the country will be 1,50,000 rooms by 2010 of which more than 1,00,000 will be in the budget category. The main reason for the shortage of hotels is the short supply of land suitable for construction hotels, particularly budget hotels. Also, land prices have shot up to astronomical levels and in many cities.

India is currently experiencing robust inbound tourism growth from many countries including Turkey. The Incredible India campaign over the past four years has now started seeing results. A number of international events in the country including the Commonwealth Games scheduled for October 2010 are likely to enhance tourist inflow into India.

India’s schedule of GATS commitments cover tourism with private participation and foreign investment permitted in many non-core areas and activities including hospitality (tourism and catering); although restrictions remain on travel agency, hotel and tourist guide services.AIR SERVICES

Domestic aviation sector in India has been expanding very rapidly despite high fuel costs. India has more than 300 airports of which at least 10 cater to regular international traffic. Areas for further potential future bilateral cooperation include airport development and pilot training.

FDI with 100% foreign equity participation is allowed with automatic approval for greenfield airports. Prior permission of the government is needed for FDI beyond 74 per cent in existing airports. The ‘open skies’ policy for liberalisation focuses on tourism. Airports managed by the Airports Authority of India (AAI) have seen new private investors allowed to undertake ground handling. Private airports have seen limited competition being made mandatory.

AAI has well established training colleges at Delhi, Allahabad and Kolkata imparting training on airport management, CNS (Communication, Navigation and Surveillance) maintenance, air traffic control, and fire services procedures. AAI colleges would be interested to provide training to aviation personnel in both countries.CONCLUSION:

Finally to conclude that, the service sector is very important for India, as it is contributing half of the GDP growth in the Indian economy. Employment is increasing due to development of service sector. There is a very good scope to improve further in the services provided by the companies and government. As India is developing very fastly there is a need for change in the quality and also the speediness of the services.REFERENCES:

www.planningcommission.nic.in/aboutus/committee/

www.economictimes.indiatimes.com/news/economy

http://www.iloveindia.com/economy-of-india/service-sector.html

DOWNLOAD

FREE TERM PAPER »

» »